Overall Picture of the EM-K12 field

Research Questions

- How was this field born and how is it evolving?

- What are the main business models?

- What are the innovation dynamics in this field? (inputs/outputs, timing of innovation/ disruptive or incremental innovation?)

- How does knowledge flow in this field?

- Is this field replicating models from other fields?

- How many companies?

- How much money do they make or how much money do they “move” in the American economy?

- How important is research from universities in this specific field?

- How important is public funding in this field?

- How important is private funding / venture capital in this field?

- Are there any specific public policies (from agencies, federal or state policies) that give incentives for openness or enclosure?

- What is the cost structure of the field?

- Who are the producers, the buyers, and the users?

- What is the structure of power from the production side and what is the structure of power in the demand side? E.g., who has the power to control production and demand? How is the control distributed?

Introduction

The Educational Materials Sector for K-12 in the USA can be divided into non-digital and digital solutions. "Digital solutions is a general term that describes a range of technologies used to enhance the delivery and the administration of K-12 education, including data management systems, web-based course and assessment materials, and online tutoring and professional development" (Cola et al. 2009, 1). While under the non-digital solutions for K-12 education we find textbooks and other course materials, such as educative toys and games.

It is important also to notice how the market has evolved and what strategies the actors have adopted to adapt businesses to the growing and overlapping sector of educational materials for K-12. "Since the 1990s, leading textbook publishers with longstanding relationships at state and local levels have included CDs and DVDs with their textbooks to deliver modular content, and many are now acquiring technologies that add value by incorporating assessment and analytical capabilities into instructional materials" (Cola et al. 2009, 2).

Thus, in this market, acquisitions and mergers focusing on market penetration and product diversification are the rule. Examples of this trend are Pearson’s 2006 and 2007 acquisitions of eCollege, Effective Education Technologies, PowerSchool and Chancery (announced May 2006); McGraw-Hill’s purchase of Turnleaf Solutions (announced in 2005), now part of The Grow Network; and Houghton Mifflin Riverdeep’s (HMR) purchase of Achievement Technologies.

However, niche players focused on software development have emerged alongside a "variety of small entities, many with roots in academia, [...] offering open-source instructional management systems to financially strapped school districts", as well as OERs (Cola et al. 2009, 2). In addition, "large software and communications companies such as Intel and Verizon are offering free solutions through their outreach programs to create goodwill and gain an opportunity to sell proprietary solutions" (ibid.).

In terms of traditional textbook imprints, mergers and acquisitions have resulted in a number of major educational publishing houses going extinct or becoming imprints of the major companies. The presence of few alternatives to the same players acquiring digital solutions subsidiaries, as mentioned above, can be traced to economies of scale "from paper to printing" favoring large enterprises (Sewall 2005). A nationally competitive company must be "capital intensive" and "full service", meaning "it must offer study guides, workbooks, and technology, along with discounts, premiums, and an array of teacher enticements"; and in states like California and Texas, "Spanish versions of texts, as well as teachers' editions, binders, and answer keys may determine which books are adopted" (ibid.).

Consolidation and need for capital intensive business practices is a result, in part, of the role financial investors have played in educational publishing since the 1970s (Thornton and Ocasio 1999); and now they are major actors in the digital education market by definition. Since 2002, Houghton-Mifflin has been owned by financial investors, more recently bought by HM Rivergroup in 2006 "from a consortium that included Thomas H. Lee, Bain and Blackstone"; in 2007, Edge Acquisition LLC bought Educate Inc., the parent company of Sylvan Learning, Catapult, and Hooked on Phonics, while Apax Learning and OMERS Capital Partners bought Thomson Learning and renamed it Cengage" (Cola et al. 2009, 4-5). Cengage focuses on higher education, but is arranging a deal with HMR "to distribute its college texts to high school honors and advanced placement courses" (ibid., 5).

Digital Solutions Market

The Digital Solutions market is a growing market, marked by fragmentation and overlapping segments, making it difficult to find specific information. The 2000 Merrill Lynch study "The Knowledge Web" estimated the market to be $1.3 billion at that time. In 2008, the market was estimated in between $5 and $7 billion Cola et al. 2009, 1.

As mentioned earlier, three market segments are identifiable under the category of Digital Solutions for K-12:

- Instructional Materials and Assessments: CDs and DVDs, and comprehensive or adaptive courseware

- Data Management and Analysis: "analysis and reporting tools that help educators modify lesson plans during the year by linking assessment results with prescribed interventions and relevant instructional materials" (Cola et al. 2009, 3); sub-sectors include student information systems (SIS), which "help schools to manage student data, track attendance, monitor schedules and store relevant information such as student demographics", and instructional management systems (IMS), which "are integrated platforms that help teachers create a collaborative learning environment that combines classroom and web-based instruction" (ibid.)

- Support Services: "professional development products for teachers and administrators, and online courses and tutoring" (ibid.)

Table on Digital Education Solutions for K-12

{kind=link}

For the purposes of this research, we will focus on only those digital solutions products that have specific educational purposes, where knowledge is embedded in a form that can be enclosed by some form of intellectual property. Thus, we will not consider products such as SIS or professional development products for teachers and administrators. However, it is relevant to point out the importance of these for market strategies leading to, for instance, "one stop and shop" arrangements and how these strategies may lead to closedness or openness in this sector.

Key drivers of growth in digital solutions have been the ongoing impact of the No Child Left Behind Act (NCLB), improving IT infrastructure in schools, and the growing number of tech-savvy students and teachers. Referring to NCLB's focus on standardized testing, "[p]ressure on schools to ensure their students achieve baseline proficiency on these tests has spurred demand for software that enables interactive, customized instruction and intervention" (Cola et al. 2009, 2). This trend has come in tandem with "a steady decline in the number of students per Internet-enabled computer", allowing school districts to take full advantage of digital educational solutions on offer (ibid.).

The Textbook Market in K-12

- Diane Ravitch, author of The Language Police, states that: "The main problem of textbooks, we know, is their quality. They are sanitized to avoid offending anyone who might complain at textbook adoption hearings in big states, they are poorly written, they are burdened with irrelevant and unedifying content, and they reach for the lowest common denominator. As a result of all this, they undermine learning instead of building and encouraging it."

- Sector sales:

- In 2004, four multinational conglomerates â Pearson, McGraw-Hill, Reed Elsevier, and Houghton Mifflin â chalk up a total of about $3 billion in elhi sales and account for roughly 70 percent of all K-12 textbooks sold.

- In 2006 the market shrank 5% from the previous year, making it one of the worst years since 2002 for the for elhi publishing sector.

- The the Association of American Publishers predictions, for the year of 2007, by was a 4.3% growth

- "The biggest sellers are reading and math books, sold as multi-volume programs for the lower grades" (Sewall 2005).

- K-12 dependency on textbooks:

- Gilbert Sewall argues that the "commercial appeal of school publishing is its reliability [...;] publishers have the opportunity to create high-margin revenue streams that can last for years" (Sewall 2005)

- A 2002 survey found that 80% of elementary and high school teacher use textbooks in their class; and almost 50% of student time in class was spent using the textbooks (Fordham, 2004). Some reports give a much higher chunk of time for textbook-centered activities: "Shadow studies that track teachers' activities have shown that between 80% and 90% of classroom and homework assignments are textbook-driven." (Jones, 2000)

- Mainly in the adoption states, teachers see themselves pressured by the school's direction to use just the adopted materials or to choose from a list;

- Many teachers lack the time or wherewithal in order to adopt other textbooks or resources;

- Some may not have a solid foundation of knowledge or may be teaching "out of the field".

Demand Structure in K-12

State adoption agencies - in the Adoption States - and Districts and its schools - in the Open States - are the main customers of the K-12 Publishing Industry. States spend relatively little on K-12 textbooks: from a high of 2.3 percent of total education expenditures to a low of 0.5 percent, according to the Association of American Publishers’ school division. On average, states spend 0.95 percent of their education budgets on textbooks â not quite a penny of every educational dollar.

A dysfunction system: the textbook adoption process

The textbook adoption process, in place in at least twenty-one states, is a statewide process where a central textbook committee or the state department of education review textbooks according to state guidelines and mandate specific textbooks and educational materials that all public schools in a certain state must use, or lists of approved textbooks and educational materials that these schools must choose from. Some of these states allow schools to buy other materials with non-state money. The states that do not hold adoption processes are called Open Sates.

The majority of the adoption states are the in south and west, while open are concentrated in the east and north.

However, since publishers naturally want to make their textbooks available in as many schools as possible, amortizing their costs and keeping up with quarterly sales goals, the adoption states that regulate textbooks effectively determine their content nationwide, particularly the huge adoption states of California, Texas, and, in a lesser sense, Florida:

"The twenty-one states that currently have statewide adoption policies are mainly in the South and West and are dominated by California, Texas, and Florida, which account for as much as a third of the nation’s $4.3 billion K-12 textbook market. Few el-hi textbook publishers can afford to spend millions of dollars developing a textbook series and not have it adopted in these high-volume states."(Fordham, 2004. p. 19)

A report presented by The Thomas B. Fordham Institute, 'The Mad, Mad World of Textbook Adoption', concludes that:

- Textbook adoption has been hijacked by pressure groups;

- Textbooks are now judged not by their style, content, or effectiveness, but by the way they live up to absurd sensitivity guidelines;

- The adoption process encourages slipshod reviews of textbooks written by anonymous development houses, according to paint-by numbers formulas;

- Finally, textbook adoption created a textbook cartel controlled by just a few companies. (Fordham, 2004)

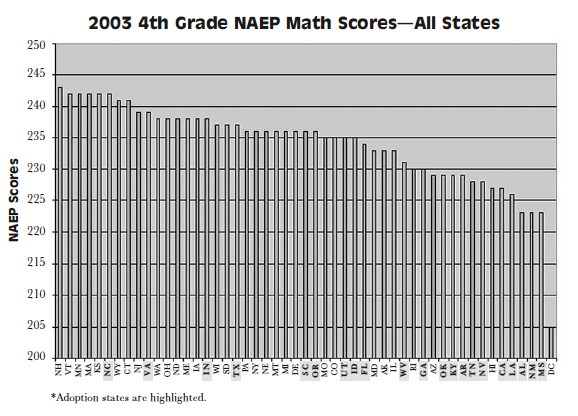

Adoption x Open Territory States

This chart on 4th grade math scores shows better score achievement among the open states. The same situation happens in reading and in math and reading in the 8th grade. (Fordham, 2004)

{kind=link}

Consequences: A conspiracy of good intentions

- Many are the consequences of the adoption process.

- Publishing practices:

- "But by that time, publishers themselves had learned to anticipate the objections that California might raiseâand had formulated their own bias/sensitivity guidelines. In effect, publishers agreed to censor their own textbooks before they showed them to state officials."(Fordham, 2004. p. 11)

- Quality:

- Today's most marketable textbooks are often not the work of committed scholars who want to explain the intricacies of their subject in the most engaging way. Instead, Whitman says, "textbooks are hurriedly put together by teams of hack writers from 'development houses,' known as 'chop shops.' Publishers are preoccupied with scrubbing textbooks of any references that adoption panels in California and Texas might object to." (Fordham, 2004). Practices of censorship are currently, part of the publishing process, in order to win contracts from state education departments in the big adoption states.

- Impact of curriculum on achievement:

- "textbook content in different nations correlated closely to what their children learnedâand how they fared on tests. U.S. math and science textbooks were hundreds of pages longer than those in other lands. But they were so dumbed down, and flitted so relentlessly from topic to topic, that American schoolchildren were learning less than their peers."(Fordham, 2004. p.2)

- "In other textbook-heavy areas of the curriculum, particularly history, the performance of American schoolchildren is every bit as disappointing. In both 1994 and 2001, more than half of high school seniors scored “below basic” â the lowest outcome possible â on the National Assessment of Educational Progress in U.S. history." (Fordham, 2004. p.2)

- Regarding "serving the user needs"

- In addition,in the K-12 textbook market, the customary feedback loop between manufacturer and user is missing. Former congresswoman Pat Schroeder, who until 2008 was the head of the Association of American Publishers, defended elhi publishers in a television interview, pointing out that they are only following the time-honored business model, “The customer is always right.” However, the problem with the K-12 textbook market is that the customers and buyers (i.e., the state adoption agencies) aren’t the actual consumers (i.e., teachers and students).

- Regarding non-adoption states

- Publishing practices:

Most influential adoption states:

Input Innovations

Writing-for-Hire

"Companies have shrunk their editorial and production staffs and [...] they are [...] abandoning the royalty-based author system. Some new secondary-level history textbooks have no authors at all. Authors have been replaced by a long list of contributors, censors, and special pleaders, concerned first of all that history meets their particular goals." (Sewall 2005)

Bibliography for Item 2 in EM

Back to The K-12 Level

Back to Educational Materials